Mobilizing 43 billion euros! Is Europe’s semiconductor industry making a comeback?

Europe was once an important origin of early development in the global semiconductor industry, with top-notch technological capabilities and manufacturing capacities. Semiconductor industry giants like Infineon, STMicroelectronics, NXP, and ASML, which holds a monopoly position in the lithography machine market, are all European companies. However, subsequent operational decisions by European enterprises directly led to their fall from the pinnacle of the semiconductor world.

Chip Manufacturing Capacity: One-Quarter to One-Tenth of Global Total

0 1

In the 1990s, Europe held a 44% share of the global chip market. However, around 2005, European semiconductor manufacturers began relocating their supply chains to East Asia in search of investment opportunities and to reduce labor costs. As a result, their market share gradually shrank, and their manufacturing capabilities fell behind. While the global semiconductor industry prospered for a long period, Europe’s share of global capacity dropped from 24% in 2000 to the current 10%.

Since 2021, the European Union has experienced a severe “chip shortage” in its semiconductor supply. Chip shortages or even disruptions have threatened the normal operations of various industrial sectors and even strategic security departments.

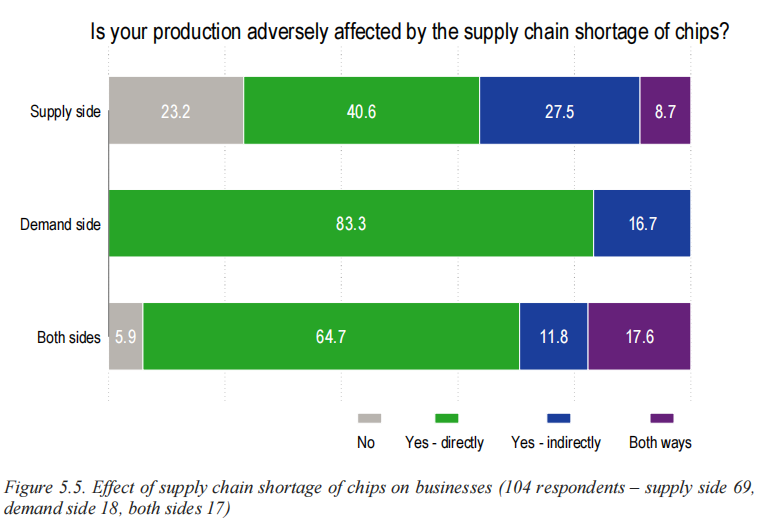

The European market is affected by the chip supply shortage, source: European Chip Survey Report.

The chip crisis in the European Union is a microcosm of the global semiconductor chip shortage, resulting from the combined effects of various factors. The European political, business, and academic circles generally believe that the most significant factor is the structural flaws in the European Union’s semiconductor ecosystem. Its vulnerability is unable to cope with the adverse impacts of global semiconductor supply chain fluctuations.

On one hand, the value chain layout of the European Union’s semiconductor industry is highly imbalanced. European Union companies have relatively weak capabilities in digital logic (processors and memory) design and primarily invest in the early stages of research and development, with most of the research outcomes being industrialized outside the European Union. On the other hand, the global semiconductor industry is built upon a collaborative system of interdependence, relying on specialized capabilities in different geographic regions. Despite European Union companies holding significant positions in the semiconductor value chain, they still heavily depend on a few external suppliers for materials, design, manufacturing, packaging, testing, and assembly. The European Union lacks the flexibility and self-sufficiency to effectively address the global chip shortage crisis.

It is for these reasons that European Union authorities analyze that there are structural flaws in the European Union’s semiconductor value chain. It is imperative to leverage public resources from the European Union and its member states, as well as the power of stakeholders in various markets, to take strong collaborative actions and comprehensively and effectively address the semiconductor supply shortage crisis.

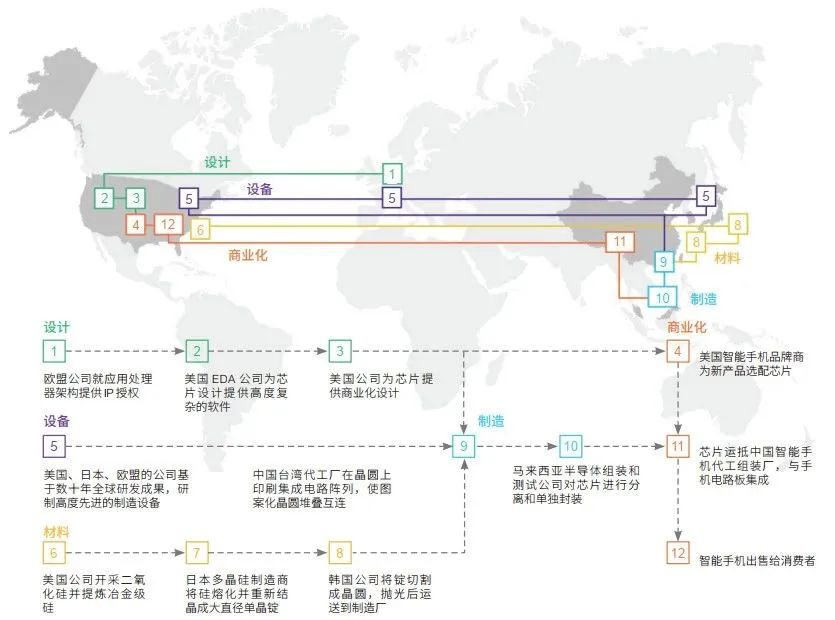

Geographical Footprint and Collaborative Processes in the Global Semiconductor Supply Chain

(Using the example of semiconductor chips required for American branded smartphones)

Source: Chinese Academy of Sciences

Against this backdrop, the European Union announced its long-anticipated “European Chip Act” in February 2022. On July 25th of this year, the Act was approved by the European Council and is now awaiting signature to come into effect.

According to the package of measures disclosed, following the enactment of the “Chip Act,” the European Union plans to mobilize 43 billion euros in public and private investment (including allocating 3.3 billion euros from the EU budget). The intention is to raise the EU’s global market share of chips from its current under 10% to 20% by 2030. Furthermore, the EU will establish capability centers to attract talent and drive chip research and development; set up a chip export monitoring mechanism to address potential supply crises; and encourage member states to support chip production and entrepreneurship, creating conditions for establishing a chip production base in the EU.

Various regions are attracting the return of industries, further complicating Europe’s development challenges.

02

In fact, it’s not just the European Union; an increasing number of countries are realizing that without a complete industrial chain, achieving technological innovation becomes challenging. As a result, many countries are continuously strengthening their local manufacturing industries. Taking the United States as an example, in recent years, the U.S. has introduced regulations and measures such as the “Reducing Inflation Act” and the “Chip Science Act” to attract the reshoring of manufacturing. Enterprises that were previously positioned in Asia and Europe are gradually bringing their industries back to the United States. This trend is particularly evident in the chip industry.

According to compiled reports from foreign media, since August of last year, about one-third of the committed investment to the U.S. comes from companies headquartered outside the United States. Among them, investments from South Korea and Japan make up the majority of non-U.S. investments. As of April this year, more than 75 manufacturing projects with a value of over $100 million each have been announced, mainly focused on semiconductor, electric vehicle, battery, and clean energy component manufacturing.

Apart from the participation of ally companies from South Korea, Japan, and others, the U.S. has also attracted investments from European enterprises.

Previously, there were reports that the UK semiconductor company Pragmatic Semiconductor had begun operations in the United States. The company’s filings indicate that it established a company in the U.S. in February of this year. In addition to Pragmatic Semiconductor, chip companies like IQE and Paragraf are actively seeking subsidies in the U.S., intending to build factories there, and even considering relocating their headquarters to the other side of the Atlantic.

Image source: ShutterStock

With the outflow of local enterprises, the pressure on the European semiconductor industry has become even more pronounced on top of its existing challenges. Since 2020, following the disruption of global supply chains caused by the pandemic, the global political and economic situation has become increasingly complex. Europe is facing geopolitical conflicts and energy crises on one hand, while dealing with the draining of its industries by overseas actors on the other. This has accelerated the loss of Europe’s industrial base and brought significant effects to the European semiconductor industry chain that cannot be ignored.

In March 2023, Europe released the “Critical Raw Materials Act” to ensure that Europe can secure safe, diverse, affordable, and sustainable supplies of critical raw materials, further revitalizing domestic industries and promoting related investments.

At the time, scholars analyzed that “if Europe does not strengthen protection and propose offensive measures, it will further lose its comparative advantages in the future. Consequences include technological loss, control of critical raw materials by some countries, and being forced to pay economic and political costs.”

This time, the European announcement of the “European Chip Act” highlights protectionism in its full form. Compared to the U.S. “Chip Act,” which focuses on restraining the development of semiconductor industries in other countries, the European Act emphasizes enhancing the resilience of the local chip supply chain, technological competitiveness, and crisis response capabilities. This means boosting the EU’s innovation capabilities in advanced chip design, manufacturing, packaging, and the entire industry chain, as well as cutting-edge and next-generation chip innovation capabilities.

The determination of Europe is evident, but does it benefit China?

03

However, while Europe has shown determination in the semiconductor field and has plans for implementation, its limitations are also evident.

Firstly, the current state of development in the European chip industry is lagging behind, and structural issues are prominent, making comprehensive catching up a challenging task. McKinsey & Company once predicted that Europe would need a decade to manufacture chips that are comparable to those of leading players in Asia and the United States.

Moreover, building the capability of the European chip industry requires long-term political will, significant policy support, and resource investment. In terms of the implementation of the “European Chip Act” itself, the high investment amount and potential risks may lead to insufficient confidence among public and private sector investors. Additionally, due to the unique nature of the EU system, the implementation of the Act will involve significant coordination among member states, posing challenges that should not be underestimated. Furthermore, surveys have shown that the introduction of chip acts in Europe and the United States signifies their departure from free-market principles toward “managed intervention,” which contradicts the industrial policies they have opposed in the past. The ultimate effects might fall short of expectations.

While Europe’s efforts are commendable, there are considerable hurdles to overcome, and the success of such initiatives will require sustained commitment, significant resources, and careful navigation of complex political and economic landscapes.

Reports have already suggested that the introduction of the European Chip Act could potentially benefit China. The chip act proposes a “chip diplomacy” initiative that calls for the European Union to cooperate with strategic partners that share similar ideals, including the United States, Japan, South Korea, and Taiwan (China), to enhance supply security, address supply chain disruptions, and strengthen dialogue and coordination in areas such as chip raw materials and third-country export controls. This could increase the demand for Chinese chip products, as China has consistently been one of the world’s largest semiconductor markets. European Union companies may seek more cooperation opportunities in the Chinese market. Additionally, European chip manufacturers might choose to relocate some of their production to China to avoid the increased costs due to trade barriers. This could stimulate the development of China’s chip industry and promote the improvement of related supply chains.

Generally, the establishment of a company’s factory depends on several factors: raw materials, labor force, market, and policies. Compared to Europe and the United States, China’s industrial chain is more complete, the market is enormous, and conditions like raw materials and labor are abundant, providing a significant advantage.

While previously following U.S. policies, companies like TSMC and Samsung set up factories in the United States, the results indicate that the subsidies promised by the U.S. are hard to attain, talent shortages are an issue, operating costs have significantly risen, and the future development situation is uncertain.

Recently, European semiconductor companies have already pledged investments in China. On June 7th, the second-largest European chip manufacturer, STMicroelectronics, signed an agreement with Sanan Optoelectronics to jointly build a silicon carbide device factory in Chongqing. It’s understood that this mega-factory, costing about 22.8 billion RMB, will gradually start production in 2025, with the industrial chain reaching maturity by 2028. The factory will be able to produce at least 10,000 8-inch silicon carbide wafers per week. After chip production, the chips will be sold directly to STMicroelectronics by the factory.

STMicroelectronics’ silicon carbide manufacturing factory. Image source: Huanqiu Defense.

With the introduction of the “European Chip Act,” what kind of impact does it have on China? Sun Chenghao, a scholar from the Center for Strategic and Security Studies at Tsinghua University, expressed in an interview with the Global Times that the European Union’s issuance of the chip act, in pursuit of “strategic autonomy” in the field of technology, presents both opportunities and challenges for China. The EU’s pursuit of “strategic autonomy” helps maintain the independence of the EU’s policy towards China and promotes genuine independent development of its relations and cooperation with China.

Source: Translated from Tencent News, Chip Master Official Account, August 6, 2023

{kind=link}